Mumbai’s real estate market is a marvel — and a paradox. It stands among the world’s most expensive cities to own property, yet it remains plagued by affordability crises and housing shortages. The reason isn’t just the invisible hand of supply and demand. It’s a deliberate architecture, shaped and steered by government policies, taxes, and levies At the heart of this system lies the Ready Reckoner (RR) rate — a single number that influences the cost of construction, approvals, and ultimately, the price a homebuyer pays. In Mumbai, the government isn’t merely an umpire setting the rules; it is the largest stakeholder, extracting a substantial share from every real estate transaction.

The City of Dreams is booming once again — but behind the boom is a silent reality: homeownership in Mumbai today is taxed, tariffed, and traded more by policy than by the market, writes TITTO EAPEN.

UNDERSTANDING READY RECKONER (RR) RATES: THE INVISIBLE HAND IN PRICING

The Backbone of Mumbai’s Real Estate Valuations

The Backbone of Mumbai’s Real Estate Valuations

In Mumbai’s dense and intricate real estate ecosystem, the Ready Reckoner (RR) rate is far more than a technical benchmark — it is the backbone upon which property valuations, taxes, premiums, and even project viability are built. Issued annually by Maharashtra’s Department of Registration and Stamps, the RR rate sets the minimum value for property registration. In theory, it ensures transparency and curbs underreporting. In practice, it acts as a foundational driver of costs across the value chain. Every adjustment in RR rates immediately impacts the stamp duty payable by buyers and the premiums charged to developers. This invisible recalibration not only determines the final price tag of apartments but also dictates how viable new projects can be.

From Regulator to Stakeholder: The Government’s Expanding Role

What was once meant to be a tool for curbing black money has now transformed the government into the largest stakeholder in every real estate transaction. Premiums for additional Floor Space Index (FSI), open space deficiency charges, development charges, fungible area premiums, and even approvals for environmental and fire compliances are linked to the RR value. Developers like Dhaval Ajmera of Ajmera Realty estimate that 30% to 40% of a project’s overall cost is now attributable to government premiums — a proportion set to rise further with every revision. “The incremental increase is expected to significantly affect construction costs and premium charges,” Ajmera noted. The burden is inevitably transferred to the end consumer, squeezing affordability further.

The 2025 Hike: Modest on Paper, Massive in Impact

In April 2025, the Maharashtra government announced a statewide average RR rate hike of 3.89%, with Mumbai’s figure standing at 3.4%. While the government framed the revision as moderate and necessary for revenue targets — Maharashtra’s property registration revenue crossed ₹57,000 crore in FY2024–25 — the industry’s reading is starkly different. Chintan Sheth, Chairman and MD of Sheth Realty, pointed out that the timing of the hike could not have been worse. “Sales are already showing signs of slowing down in 2025.

Developers are facing sharp rises in construction costs. This increase doesn’t seem like the right step from the government’s side,” Sheth observed. Industry leaders argue that the real impact of an RR rate revision isn’t linear — it triggers a cascading rise across multiple cost heads, eroding affordability at every level.

The Double Burden: Taxes, Levies, and RR-Linked Premiums

What further complicates the situation is that the RR-linked ecosystem is layered on top of other government-imposed charges: The 1% Metro Cess, steep fungible premiums, open space deficiency penalties, and high environmental clearances all add to the mounting cost base. Niranjan Hiranandani, Chairman of NAREDCO, emphasized that the RR hike, without factoring in these cumulative pressures, risks making redevelopment projects financially unviable. “Development expenses, additional FSI, and municipal charges are all tied to it. The absence of GST consideration in RR rates further aggravates redevelopment costs,” he stated. The result is that Mumbai’s real estate inflation today is not just a function of market scarcity or construction difficulty — it is increasingly a result of systemic, policydriven cost-push pressures.

The Bigger Question: Is the System Sustainable Anymore?

The fundamental debate is no longer about whether RR revisions are justified based on market movements. The larger question is whether the government’s growing fiscal reliance on property taxes, premiums, and RR-linked revenues is sustainable — or whether it risks permanently pricing out Mumbai’s aspiring homebuyers.

THE GREAT MUMBAI REAL ESTATE BOOM: A DOUBLE-EDGED SWORD

Record-Breaking Sales, Record-Breaking Costs

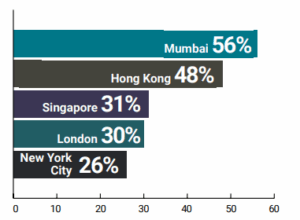

Mumbai’s real estate market has witnessed a historic boom over the past three years. According to data from Knight Frank India, housing sales in Mumbai Metropolitan Region (MMR) crossed 1.2 lakh units in 2024 alone — an all-time high. The luxury and ultraluxury segments, in particular, expanded by over 18% yearon-year, driven by a surge in post pandemic wealth creation and a growing appetite for marquee addresses. At the same time, property prices have risen sharply. Knight Frank’s Affordability Index notes that Mumbai’s average price-to-income ratio now stands at 56%, meaning more than half of a family’s monthly income would be needed just to service a standard home loan. By global comparison, this makes Mumbai less affordable than London, Singapore, or New York. However, this sales surge has masked an uncomfortable truth: much of Mumbai’s housing growth is concentrated in the premium and luxury categories, not in the mid-income or affordable segments where the bulk of demand exists.

The Premium Trap: When Growth Becomes Exclusionary

As property prices rose, so too did the reliance on RR rates and government premiums for revenue generation. Today, the premium payable to government agencies can constitute up to 35–40% of the project cost in prime Mumbai locations — a figure unheard of in most global markets. According to a recent CREDAI report, developers in Mumbai pay more in government premiums than in any other Indian city, including Delhi NCR, Bangalore, or Hyderabad. This creates what economists call a “premium trap” — a structural distortion where real estate becomes increasingly expensive not purely because of demand or scarcity, but because of cascading state-imposed costs. Dhaval Ajmera’s observation that “30–40% of a project’s cost is linked to government premiums”is not an exaggeration — it is now the industry standard.

The Paradox of Booming Supply and Shrinking Affordability

At first glance, Mumbai’s skyline is booming with cranes, towers, and redevelopment sites. The city recorded more than 600 new project launches in 2024, according to Anarock Research. Yet despite the flood of new supply, the affordability crisis has worsened. In fact, the median home size in Mumbai — already the smallest among Indian metros — shrank by 7% between 2022 and 2024, as developers tried to keep unit ticket sizes “affordable” in absolute terms even as per-square-foot rates climbed. Meanwhile, the share of homes priced under ₹1 crore, once the backbone of the city’s housing market, has shrunk to below 30% of all sales — a sharp decline from over 50% just five years ago. Clearly, the city is building more — but it’s not necessarily building for the middle class.

Who Really Gains from the Boom? The popular narrative often frames Mumbai’s real estate boom as a win for developers and investors.

In reality, however, the government’s role as the biggest financial beneficiary is increasingly evident. Maharashtra’s property registration collections — boosted heavily by RR rate hikes and associated premiums — grew by 11% year-on-year in FY24–25, topping ₹57,422 crore. In many redevelopment projects in the city’s prime zones, government levies can total ₹7,000–₹9,000 per square foot, making them a larger cost component than even raw land or basic construction costs. As Domnic Romell, MD of Romell Group, rightly pointed out, while the recent RR rate revision was balanced, the absence of GST integration into redevelopment premiums remains a major oversight. The tax system’s inefficiency not only inflates project costs but reduces the scope for price moderation — a missed opportunity to balance fiscal needs with housing policy objectives.

The Risk of a Demand Slowdown: A Fragile Boom

Signs of stress are beginning to appear despite record sales. According to a PropEquity report, Mumbai’s unsold inventory rose by 7% in Q1 2025 compared to the same period last year, especially in the ₹2–5 crore segment. With EMIs rising, project approval delays

compounding financial costs, and fresh launches targeting only the upper end of the market, industry players warn of a potential slowdown brewing underneath the surface. As Sachin Mirani of Squarefeet Group warned, escalating RR rates threaten the “Housing for All” vision by pushing properties above the ₹45 lakh affordability threshold.If this trend continues unchecked, Mumbai’s boom could morph into a high-end bubble — disconnected from the broader demographic realities of the city.

HOW THE GOVERNMENT BECAME THE BIGGEST STAKEHOLDER IN MUMBAI’S REAL ESTATE MARKET

From Regulator to Revenue Maximizer

In most global cities, the government’s role in real estate is confined to zoning, regulating construction norms, and facilitating infrastructure. In Mumbai, however, the government has positioned itself not just as a facilitator but as a major financial stakeholder — and increasingly, the largest beneficiary of the real estate value chain. Across every transaction — whether it is buying a home, transferring land, seeking project approvals, or acquiring additional development rights — the state claims a significant share through a combination of Ready Reckoner (RR) linked charges, premiums, and taxes.

The Numbers Behind the

Government’s Dominance

Consider the anatomy of a typical residential project in Mumbai today:

- Stamp Duty and Registration Fees: 6%–7% of the property value, based on RR rates.

- Fungible FSI Premiums: 35% of the construction area, calculated at a percentage of RR value.

- Open Space Deficiency Charges: Levied at 10–15% of RR value in many urban zones.

- Development Charges, Approval Fees, Fire NOC, Environmental Clearances: Almost all indexed to the RR rate.

- Additional Charges: 1% Metro Cess added to stamp duty, pushing the transaction cost even higher.

When added together, government-imposed premiums and taxes account for 30–40% of the total project cost — a figure unheard of in major cities globally. Developers like Boman Irani of Rustomjee Group have pointed out that while RR revisions are “judicious,” they must be accompanied by rationalization of construction-related costs. Otherwise, he warned, the rising burden ultimately filters down to the buyer. In high-density zones like South Mumbai, industry estimates suggest that for every ₹100 earned from a home sale, ₹40–₹45 flows to government coffers through direct and indirect levies.

Premiums Outpacing Private Profits

In a revealing analysis by Anarock Property Consultants, it was found that in certain Mumbai redevelopment projects the premiums paid to the municipal corporation and various state agencies exceeded the developer’s own profit margin. Effectively, the government earns more from every apartment sold than the builder who assumed the project risk. This distortion is further amplified by the fact that even basic amenities now attract government premiums. Want to build a podium garden? Pay a fungible premium. Want to build a clubhouse? Pay additional charges. Want extra parking floors? Pay again all benchmarked to RR values, not actual construction costs. Such a system incentivizes revenue extraction over affordability creation.

The Inflationary Spiral: Policy-Induced, Not Market-Induced

One of the most dangerous outcomes of this model is that Mumbai’s property inflation is increasingly policy-induced, not market-induced. Every incremental hike in RR rates fuels a proportional rise in premiums and levies, creating an inflationary spiral that operates independently of real demand-supply dynamics. Dhaval Ajmera’s calculation that every 5 10% rise in RR rates can add 7–12% to final project costs is already visible in recent launches, where ticket sizes have increased by an average of 8–10% in 2025, even in a cooling demand environment. As a result, the market is seeing artificial price resilience — projects are expensive not because material costs or land scarcity alone dictate it, but because policy mechanisms inflate the base costs.

A Booming Market, A Hollowed-Out Affordability

Despite record transaction volumes, Mumbai’s market is hollowing out in affordability terms. The ₹45 lakh affordable housing bracket — critical for middle-class and first-time buyers — is shrinking dramatically. In satellite cities like Thane and Navi Mumbai, developers like Sachin Mirani and Rakesh Prajapati warn that revised RR rates are pushing even entry-level projects beyond the “affordable” classification, undermining the government’s stated objective of Housing for All. Meanwhile, the government’s fiscal dependence on real estate continues to deepen. Property registration and stamp duty collections now account for over 10% of Maharashtra’s total state revenues — a level of fiscal reliance that few economies in the world maintain in one sector. In other words, Mumbai’s homebuyers are not just financing private aspirations — they are underwriting the state’s financial stability itself.

An Industry Caught Between Pragmatism and Pressure

The real estate community in Mumbai has responded to the recent hike in Ready Reckoner (RR) rates with a mix of cautious acceptance, strategic concern, and outright frustration. While some developers have acknowledged the inevitability of revisions after a three-year hiatus, others warn that the rising cost structure threatens to tip the market into unsustainable territory. The divergence in opinions reflects the complexity of Mumbai’s real estate ecosystem — a market where resilience is baked into the DNA of the business, yet one where systemic pressures are slowly straining even the most experienced players.

The Pragmatists: A Necessary Adjustment, but With Caveats

Several senior developers, while acknowledging the hike, have called for a more nuanced approach to cost management. Boman Irani, Chairman and MD of Rustomjee Group, described the revision as a “reasonable and well-considered move,” appreciating the government’s attempt at a balanced adjustment. However, he was quick to point out a critical oversight: the failure to update construction cost calculations in line with modern, RERA-mandated transparency. Irani emphasized the need for categorizing construction costs based on building heights, noting that “no building in Mumbai is typically under 56 meters,” making the existing classification outdated. Similarly, Domnic Romell, MD of Romell Group, welcomed the moderate nature of the hike, but highlighted that excluding GST from redevelopment premium calculations was a missed opportunity. “Had GST been factored into the rate structure, it would have had a profound impact on redevelopment projects,” Romell observed. For these leaders, the issue is not the principle of revising rates — it is the failure to modernize the framework within which these revisions are executed.

The Cautious Critics: Warning Bells on Affordability

A second group of developers sounded alarm bells over the impact on affordability and middle-class access to housing. Dhaval Ajmera of Ajmera Realty pointed out that around 30–40% of a project’s cost in Mumbai is now linked to premiums indexed to RR rates. “Even a modest 3–4% increase in RR rates could inflate residential costs by 5–10% in real terms,” he warned, predicting a fundamental shift in cost dynamics that will be difficult for the end user to absorb. Chintan Sheth of Sheth Realty went further, questioning the timing itself. “With sales showing signs of slowing down in 2025, this increase doesn’t seem like the right step from the government’s side,” he noted. In his view, developers are being squeezed between rising material costs, regulatory premiums, and a market increasingly sensitive to price hikes. Meanwhile, Cherag Ramakrishnan of CR Realty warned that stamp duty expenses for buyers would rise in parallel, leading to a slower market as “both buyers and sellers adjust to the new pricing dynamics”.

The Alarmed Voices: Affordable Housing Under Threat

For developers focused on the mass and affordable segments, the concerns are even starker. Sachin Mirani, Director of Squarefeet Group, bluntly stated that the RR rate hike “could have a significantly negative impact on the Prime Minister’s vision of affordable housing”. In cities like Thane, where affordability margins are razorthin, even minor cost escalations can push units beyond the ₹45 lakh affordable threshold — disqualifying buyers from accessing government incentives and low-interest home loans. Jitendra Mehta of JVM Spaces echoed this sentiment, arguing that the hike would “increase construction and.

Emerging Markets Stay Hopeful, But Watchful

Interestingly, developers operating in emerging hubs like Dronagiri and Panvel showed cautious optimism. Rakesh Prajapati, President of CREDAI MCHI Dronagiri Unit, stated that although approval costs would rise, demand fundamentals remained strong in growth corridors linked to major infrastructure projects like the Navi Mumbai International Airport. “Despite the RR hike, Dronagiri remains a very attractive investment destination,” he affirmed, pointing to long-term demand drivers. However, even in these markets, developers acknowledge that escalating premiums could eventually widen the gap between investment-grade projects and genuinely affordable housing.

An Industry at Crossroads

The reactions from across the industry make one reality clear: Mumbai’s real estate developers are pragmatic enough to work within evolving regulatory frameworks — but they are also acutely aware that the cumulative weight of rising RR rates, premiums, and taxes is testing the structural limits of the market. Unless there is a broader realignment between fiscal ambition and affordability imperatives, the resilience of Mumbai’s housing market — so often celebrated — could give way to deeper systemic vulnerabilities. The next battleground, it seems, is not just market forces, but policy frameworks themselves.

THE SPIRALING COSTS:HOW RR RATES INFLATE THE ENTIRE ECOSYSTEM

THE SPIRALING COSTS:HOW RR RATES INFLATE THE ENTIRE ECOSYSTEM

When One Number Changes Everything

In most industries, inflation is a complex dance of supply chains, labor costs, and market forces. In Mumbai’s real estate sector, however, a single figure — the Ready Reckoner (RR) rate — has the power to trigger inflation across the entire ecosystem. Because so many government charges, premiums, and levies are linked directly to the RR value, even a seemingly minor hike in the rate sets off a chain reaction that escalates every stage of the real estate process — from land acquisition to final apartment sale. In essence, the RR rate acts not merely as a reference point but as a multiplier of project costs.

The Domino Effect: From Land to Buyer

When RR rates rise, the immediate and most visible impact is on stamp duty and registration fees, both of which are calculated based on the higher of the RR rate or the transaction value. This inflates the upfront transaction cost for buyers almost overnight, making affordability an even bigger hurdle. However, the less visible — and far more devastating — impact happens upstream in the project development cycle. Premiums for fungible FSI, open space deficiency, TDR loading charges, stair/lift area compensations, and numerous environmental and fire-related approvals are all benchmarked to the RR value. Every percentage point hike in RR effectively magnifies the cost of building the project itself. Industry calculations suggest that a 3–4% rise in RR rates can lead to an 8–10% increase in final project costs once all cascading premiums and fees are accounted for. Dhaval Ajmera’s warning that “construction and premium charges will rise significantly, not marginally,” is already visible on ground — with several developers now recalibrating project feasibility models before launching new phases.

Shrinking Apartments, Rising Costs

The most common developer strategy to absorb these rising costs without alienating buyers has been reducing apartment sizes. According to data from ANAROCK, the average apartment size in MMR shrank by 7% between 2022 and 2024. But this tactic has its limits. At a certain point, shrinking apartment sizes degrades living standards, particularly in the mid-income and upper mid-income segments that form Mumbai’s aspirational core. Already, homebuyers in Mumbai get the smallest apartments for the highest prices compared to any other major Indian city — a unique inversion of value proposition that erodes long-term demand sustainability.

Impact on Project Viability

For developers, rising premiums linked to RR rates don’t just affect pricing — they directly threaten project viability. In redevelopment-heavy micro-markets like Bandra, Andheri, Dadar, and Mahim, where margins are already thin due to tenant rehabilitation obligations, the additional burden of inflated government premiums can make projects financially unfeasible. As Domnic Romell pointed out, the lack of GST adjustment into redevelopment premium calculations has further complicated cost structures. Without offsetting benefits, many redevelopment projects could face viability crises, slowing down the very urban regeneration that Mumbai critically needs.

Affordable Housing — The First Casualty

Perhaps the most tragic consequence of the RR rate spiral is its impact on affordable housing stock. Sachin Mirani’s warning rings loud: the increase in RR rates risks pricing affordable projects out of their eligibility bands. A ₹40–₹45 lakh home, already difficult to deliver under current cost pressures, becomes virtually impossible once RR-linked premiums rise by another 8–10%.

MUMBAI VS THE WORLD: A PRICING ANALYSIS

MUMBAI VS THE WORLD: A PRICING ANALYSIS

A City That Outpriced Its Own People

Mumbai’s real estate boom has often been celebrated in narratives of economic resilience and entrepreneurial spirit. Yet when measured against global benchmarks, Mumbai’s housing affordability paints a much starker picture — one of a city that has systematically priced out its middle class, not merely through market forces but through policy structures that amplify inflation. When adjusted for income levels, Mumbai today ranks as one of the least affordable cities in the world — consistently beating even notoriously expensive markets like Hong Kong, London, and New York.

The Price-to-Income Gap: A Global Outlier

According to Knight Frank’s 2024 Affordability Index: Mumbai’s Home Price to Income Ratio: 56% (i.e., over half a household’s income goes toward servicing a standard home loan)

Simply put, buying a home in Mumbai today demands a greater sacrifice of household income than in almost any other global financial hub. This gap persists despite Mumbai’s average per-square-foot prices being lower than Manhattan or Central London — because Mumbai’s average household income remains significantly lower while transaction taxes and government premiums remain disproportionately high. Thus, it is not just a question of high prices — it is a structural problem of high taxation layered onto lower incomes, compounding the affordability crisis.

Simply put, buying a home in Mumbai today demands a greater sacrifice of household income than in almost any other global financial hub. This gap persists despite Mumbai’s average per-square-foot prices being lower than Manhattan or Central London — because Mumbai’s average household income remains significantly lower while transaction taxes and government premiums remain disproportionately high. Thus, it is not just a question of high prices — it is a structural problem of high taxation layered onto lower incomes, compounding the affordability crisis.

The Hidden Cost of Ownership: Government Levies vs. Global Norms

In most global cities, government-imposed transaction costs (including registration, taxes, and regulatory premiums) range between 5% to 8% of property value. In Mumbai, when all premiums, stamp duties, cess, and hidden levies are accounted for, the effective government share of every property transaction can touch 30–40%. This difference is not trivial. It fundamentally alters the risk-reward equation for homebuyers and developers alike, pushing both cost and risk burdens disproportionately onto private citizens while maximizing government collections. As Boman Irani emphasized, Mumbai’s current cost structure is no longer purely reflective of material and labour inflation — it is policy-driven escalation that accumulates at every level of the value chain.

The Myth of Organic Price Growth

The Myth of Organic Price Growth

While Hong Kong or Singapore’s real estate prices are driven by natural land scarcity and controlled supply frameworks, Mumbai’s price inflation is increasingly seen as policy-manufactured rather than organically market-driven. Unlike Singapore, where the Housing Development Board (HDB) actively intervenes to create affordable mass housing, or New York, where zoning incentives promote inclusionary housing, Mumbai’s policy framework systematically monetizes every square inch of buildable space without proportionate reinvestment into housing access. The lack of government-supported affordable housing supply, combined with relentless monetization of real estate development through RR-linked premiums, ensures that every market cycle in Mumbai starts from an artificially elevated cost base. As Cherag Ramakrishnan noted, the “stamp duty expenses for buyers will rise sharply” post-RR hike, slowing down even natural transaction momentum — a clear sign that structural costs, not just market conditions, are throttling growth potential.

The Bigger Risk: Global Capital, Local Displacement

Mumbai’s escalating prices are increasingly attractive to global investors seeking asset diversification — particularly in the luxury segment. However, this inflow of capital creates a risk where projects are increasingly targeted at ultra-HNIs (high-net-worth individuals) and foreign buyers, leaving the local, salaried middle-class population sidelined. In London, New York, and Vancouver, similar dynamics led to political backlash and regulatory interventions such as foreign buyer taxes and vacancy penalties. Mumbai, by contrast, continues to prioritize revenue generation over affordability safeguards — a model that, while lucrative in the short term, risks long-term social and political instability. As Jitendra Mehta warned, the current path risks creating “negative sentiment among buyers” — a euphemism for the growing frustration and alienation of local residents from the city’s own housing market.

Mumbai’s Race to the Top — And the Bottom

In global comparisons, Mumbai stands out not simply for its high prices, but for how it got there: through a compounding cycle of RR rate hikes, cascading premiums, and insufficient income adjustments. The city’s housing market is a paradox — a booming, glittering skyline built on foundations that are increasingly unaffordable, unstable, and unsustainable for the very citizens who power its economy. Without urgent recalibration of policy frameworks — not just minor tweaks — Mumbai risks achieving the dubious distinction of becoming the world’s most expensive city for everyone but its own people.

THE ROAD AHEAD: TOWARDS A MORE BALANCED ECOSYSTEM

Breaking the Cycle of Policy-Induced Inflation

Mumbai’s real estate market has always thrived on resilience. However, the current trajectory — where affordability erodes faster than incomes can rise, and systemic costs inflate independently of true demand — is unsustainable in the long run. The urgent challenge before policymakers, developers, and urban planners is clear: How to rebalance a system that rewards short-term revenue at the cost of long-term housing viability?

Breaking the current inflationary cycle will require a combination of scientific reform, regulatory rethinking, and a fundamental shift in the government’s role from revenue maximizer to ecosystem enabler.

Scientific Recalibration of Ready Reckoner Rates

First and foremost, the Ready Reckoner (RR) rate methodology itself needs urgent modernization. Currently, RR rates are updated primarily through a backward-looking assessment of registered sale prices, often missing nuances like redevelopment premiums, environmental compliance costs, and actual buyer behavior trends. Industry leaders like Boman Irani have suggested aligning RR rate calculations with RERA disclosures, which already mandate detailed cost breakdowns of construction and marketing expenses. If adopted, this would allow RR rates to reflect real-time market health rather than operate as blunt revenue-enhancement tools. Additionally, categorizing RR rates based on building typologies — such as mid-rise, high-rise, and supertall structures — could prevent distortions in construction viability across different formats, particularly in a vertical city like Mumbai.

Rationalisation and De-Linking of Government Premiums

The second, and arguably more urgent, reform is the de-linking of cascading premiums from the RR rate framework. While some baseline charges are necessary to ensure urban infrastructure funding, the current model — where multiple approvals, clearances, and FSI-related premiums are indexed to an ever-increasing RR value — leads to an unsustainable layering of costs.

A rationalisation exercise could involve:

-

Capping total government levies at a fixed percentage of project value

-

Introducing differential premium structures for redevelopment, affordable, and rental housing projects

-

Offering GST offsets or rebates on premium payments for socially desirable categories (such as affordable or senior housing)

As Domnic Romell and others have noted, the absence of GST adjustments on premiums particularly hurts redevelopment — a pillar of Mumbai’s housing renewal.

Protecting the Affordable Housing Segment

If Mumbai is serious about maintaining a socio-economic balance, policy interventions specifically targeting affordable housing are indispensable. This could include:

-

Fixed RR rates for units below ₹45 lakh to prevent affordable projects from being priced out by rate hikes

-

Priority environmental and fire clearances for affordable housing projects

-

Stamp duty waivers or reductions for first-time homebuyers in targeted segments

Without these protections, developers like Sachin Mirani warn that the affordable housing promise will remain a rhetorical ideal, not a functional reality.

A Shift from Revenue Extraction to Ecosystem Development

Finally, the government must reimagine its relationship with the real estate sector — not as a cash cow for immediate fiscal gains, but as a foundational driver of urban sustainability. Hong Kong’s public housing initiatives, Singapore’s HDB model, and even London’s inclusionary zoning policies show that strong real estate economies are built not just by enabling premium projects but by ensuring housing accessibility across demographics. Mumbai must move beyond transactional policymaking — where every policy tweak is designed to extract more — and embrace an ecosystem-based view that rewards long-term urban resilience, citizen well-being, and economic dynamism.

A Chance to Correct the Course

Mumbai’s real estate success story is too important to allow it to collapse under the weight of its own systemic contradictions. If stakeholders act now — recalibrating RR methodologies, rationalising premiums, protecting affordability, and shifting the governance mindset — Mumbai can once again become a city where opportunity is as accessible as ambition. The city’s greatest risk is not stagnation. It is allowing short-term fiscal appetite to cannibalise the very ecosystem that made Mumbai the City of Dreams in the first place. The time to rethink, recalibrate, and rebuild smarter — is now.

MUMBAI’S REAL ESTATE — AT WHAT COST?

Mumbai’s skyline today is a testament to human ambition — glittering towers stretching higher into the sky, new projects unveiling every month, and property registrations hitting historic highs. On the surface, the city appears to be in the midst of a golden era of real estate. But beneath the glamour lies a growing fracture. The soaring prices are no longer merely a reflection of land scarcity or construction costs. They are the product of a system where policy structures — Ready Reckoner hikes, cascading government premiums, and relentless transactional levies — have become as significant a driver of inflation as market demand itself.

In this new reality, the government has evolved from regulator to the single largest financial stakeholder in Mumbai’s housing economy. With stamp duties, fungible FSI premiums, development charges, and assorted taxes constituting nearly 30–40% of a project’s cost, it is no exaggeration to say that every buyer today is funding not just their home, but the State’s fiscal machinery. And yet, the affordability gap widens. The average Mumbaikar now spends a larger share of their income on housing than residents of New York, London, or Hong Kong — a paradox for a city built on the dreams of the middle class.

The risk is not immediate collapse; Mumbai’s resilience runs deep. But resilience is not infinite. If left uncorrected, the city’s real estate model will eventually cannibalise its own base — pricing out the very entrepreneurs, workers, and families that sustain its energy. The Mumbai housing dream does not have to end in exclusion. There is still time to recalibrate policies, rethink revenue models, and rebuild a market that is vibrant not just in profits, but in possibilities. Because at the end of the day, a city’s greatness is not measured by the height of its towers — but by how many of its citizens can call it home.